Interest rates set by the Bank of Canada (BoC) are important when influencing mortgage costs, home prices, and overall demand. When rates are high, borrowing becomes more expensive, often slowing price growth as fewer buyers can afford to enter the market. Conversely, lower rates make homeownership more accessible by reducing monthly mortgage payments, potentially driving up demand.

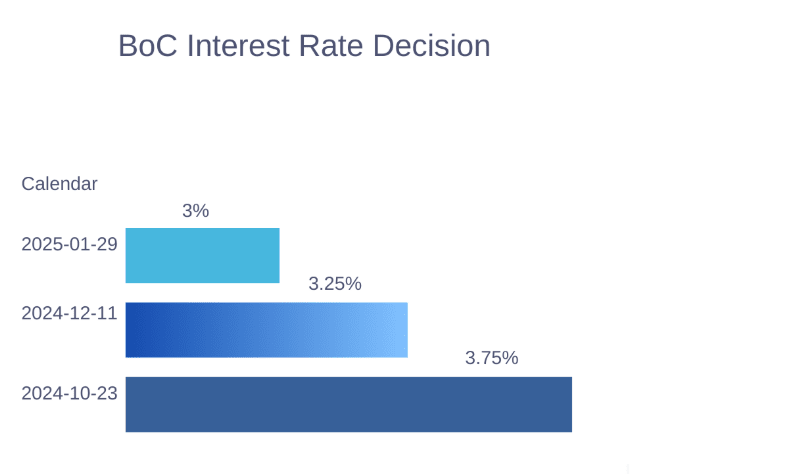

Canada’s inflation rate has now stabilized around the BoC 2% target after years of elevated price growth. This decline is largely due to previous interest rate hikes aimed at cooling demand. With inflation under control, the BoC has begun lowering rates, cutting its key policy rate to 3% in January 2025.

The latest BoC interest rate cut compared to the previous two cuts. Source: Trading Economics

Housing affordability in Canada is shaped not just by interest rates but also by income levels and supply constraints. Higher interest rates had previously slowed home price growth by making borrowing more expensive. Now, as rates decline, mortgage costs could fall, potentially increasing demand.

A key issue, however, remains housing supply. Canada has faced persistent shortages over the last decade, exacerbated by stagnating wages and increased immigration. While immigration targets have been reduced, sustained construction activity is essential to improving affordability. Without sufficient new housing, lower interest rates could reignite price increases, offsetting any benefits to buyers.

Achieving affordable housing in Canada amid these economic challenges will depend on multiple factors; however, the recent rate cut has sparked optimism among experts, who see it as a potential boost for homeownership among low- to middle-income Canadians.

Previous Interest Rates

Over the past few decades, Canadian interest rates have experienced significant fluctuations, influencing the housing market and affordability, and set the current economic conditions today.

The early 1990s were marked by high inflation, leading to interest rates peaking at 16% in February 1991. This period was challenging economically and made homeownership less accessible due to high borrowing costs.

By the early 2000s, rates had stabilized, and the economy began to grow steadily. The BoC maintained relatively low rates, encouraging borrowing and economic expansion. This period saw increased housing activity as lower rates made mortgages more affordable. The 2008 financial crisis brought about aggressive rate cuts, with rates dropping to a record low of 0.25% in April 2009. This led to a surge in housing demand as Canadians took advantage of low mortgage rates. In the following years, as the economy recovered, the BoC gradually increased interest rates, though they remained relatively low compared to historical standards. This period was characterized by steady economic growth and stable housing markets.

The 2020s brought another round of significant rate adjustments. The COVID-19 pandemic led to historic lows in interest rates, with fixed mortgage rates occasionally below 2%. This resulted in a housing boom as Canadians capitalized on cheap financing options. Starting in mid-2022, the BoC rapidly increased interest rates to combat rising inflation, with hikes as high as 100 basis points in a single decision. However, by June 2024, the BoC began cutting rates again, with a total reduction of 200 basis points by January 2025. This shift reflects efforts to balance economic growth with inflation control.

This historical context demonstrates that when interest rates are cut, mortgage rates typically follow, making borrowing cheaper. This can lead to increased demand for housing as more people can afford mortgages.

Conversely, when rates rise, borrowing costs increase, potentially reducing housing demand. The rapid rate hikes in 2022 led to higher mortgage rates, making it more challenging for some Canadians to purchase homes.

The BoC's decisions to cut or raise rates are crucial in balancing economic growth with inflation control, impacting the broader housing market. As rates continue to evolve, understanding these trends is essential for predicting future changes in housing affordability and demand.

In the current context, with rates at 3% and ongoing economic uncertainties, the housing market seems to have a positive future. The BoC's recent rate cuts aim to stimulate economic activity while managing inflation risks, which could lead to increased housing demand if borrowing costs remain favourable.

Immediate and Long Term Effects

The immediate effect of the interest rate cut is a reduction in borrowing costs for Canadians. Lenders typically respond to changes in the BoC's overnight rate by adjusting their mortgage rates accordingly. Following the January cut, most lenders reduced their variable mortgage rates by approximately 0.25% within 24 hours. This decrease provides immediate relief to homeowners with variable-rate mortgages, allowing them to benefit from lower monthly payments.

In the long term, reduced interest rates are expected to enhance housing affordability. Economists suggest that lower mortgage payments can offset potential increases in home prices driven by heightened demand. As borrowing becomes cheaper, more buyers may enter the market, which could stimulate construction and increase housing supply—factors critical for addressing affordability challenges in places like British Columbia.

However, it should be noted that the anticipated benefits may not be felt uniformly across Canada. While some markets may experience rapid price increases due to heightened demand, others may struggle with affordability issues exacerbated by stagnant wages or economic uncertainty. The BoC's recent comments regarding potential tariffs from the U.S. further complicate this landscape, as they may dampen economic recovery and consumer confidence.

It’s proven that interest rate cuts have had varying impacts on the Canadian housing market. For instance, during periods of aggressive rate reductions in the past decades, such as post-2008 financial crisis measures, there was a significant boost in home sales and prices as buyers rushed to take advantage of low rates. Despite this, current economic conditions differ; inflation has stabilized around 2%, and while GDP growth is projected at 1.8% over the next two years, concerns about external economic pressures remain.

As confidence builds among potential homebuyers, we may see an increase in market activity despite affordability challenges. The interplay between interest rates, consumer sentiment, and broader economic factors will ultimately determine how effectively these cuts translate into increased homeownership and improved affordability.

While the immediate effects of the recent interest rate cut are likely to stimulate mortgage activity and potentially increase home sales, long-term impacts will depend on various factors including economic stability and buyer sentiment.

Challenges and Opportunities

Canada's housing crisis presents a significant challenge for policymakers, homebuyers, and developers alike. Skyrocketing home prices, coupled with supply shortages and rising construction costs, have made homeownership increasingly unattainable for many Canadians. Real estate developers, facing high borrowing costs and regulatory hurdles, are slowing or halting projects, exacerbating the supply-demand imbalance. Needless to say, potential interest rate cuts by the Bank of Canada could provide an opportunity to spur development and ease affordability pressures if paired with targeted policies.

Will Lower Interest Rates Spur Construction?

Lower interest rates can make borrowing more affordable for developers and homebuyers alike. In theory, this should incentivize new construction and alleviate housing shortages. However, several factors complicate this dynamic. According to Forbes, while lower borrowing costs reduce financial barriers for builders, persistent challenges—such as high material costs, labor shortages, and slow zoning approval processes—continue to deter large-scale development. Additionally, increased demand from buyers taking advantage of lower mortgage rates could drive prices higher, offsetting affordability gains. Unless supply growth outpaces demand, rate cuts alone may not resolve the crisis.

The question can be asked: Who Benefits? Middle-class Canadians or investors? A critical concern is whether rate cuts primarily benefit low- to middle-income Canadians or favour investors and speculators. Historically, lower interest rates have fueled real estate investment, driving up property values and pricing out first-time buyers. If developers focus on luxury or investment-oriented housing rather than affordable homes, rate cuts could worsen affordability for middle-class Canadians. To counter this, government intervention—such as higher taxes on speculative purchases and incentives for affordable housing development—will be necessary to ensure broader benefits.

Government Policies and Affordability initiatives

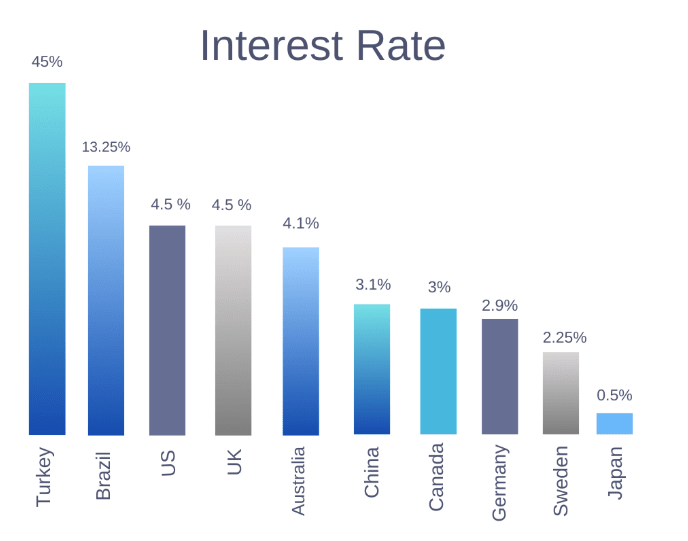

Canada's recent 3% interest rate cut will position it among the top countries with the lowest interest rates globally.

Interest Rates per country as of January 24, 2025. Source: Trading Economics

The Canadian government has implemented various measures to address housing affordability, including low-cost loans for rental housing, support for first-time buyers, and incentives for sustainable development. The Canada Rental Protection Fund and Affordable Housing Fund aim to protect tenants and boost supply. Plus, making zoning and permitting processes more efficient can accelerate housing construction, ensuring rate cuts translate into meaningful affordability improvements.

As of early 2025, Canada's average mortgage rate hovers around 5.5%, down from a peak of 7.0% in 2023. National home prices, which had surged over 40% in the previous decade, have stabilized somewhat but remain out of reach for many buyers. The Housing Affordability Index (HAI) indicates severe affordability challenges in major cities like Toronto and Vancouver, where the ratio of housing costs to household income is disproportionately high.

Before interest rate cuts, affordability was at an all-time low due to high borrowing costs and escalating home prices. With recent rate reductions, mortgage payments have declined, theoretically improving affordability.

Increased Demand for Non-Profit Housing Associations

Ultimately, the lower interest rate and increased government incentives present a positive outlook for Canadian Affordable Housing Associations and not-for-profit housing organizations, as demand is anticipated to increase.

As borrowing costs decrease, the overall housing market is likely to see increased activity. This shift creates new opportunities for Affordable Housing Associations to expand their impact. Lower borrowing costs make it more affordable for these organizations to secure loans for property acquisition, new developments, and renovations. Additionally, government funding and grants are often more accessible in periods of economic adjustment, allowing these organizations to scale their operations and enhance services.

With additional financial flexibility, many Affordable Housing Associations may also accelerate construction projects, invest in energy-efficient retrofits, or improve community services for residents. Expanding housing stock through strategic acquisitions or new builds can help meet the growing demand while ensuring long-term affordability.

Organizations with existing mortgages may also benefit from lower rates, reducing operational costs and freeing up funds for tenant support programs, maintenance, and community initiatives. Furthermore, favorable economic conditions can create new partnership opportunities between Affordable Housing Associations and private developers, enabling collaborative projects that increase the supply of affordable housing.

Looking Ahead

While lower interest rates are not a standalone solution to housing affordability, they create a strong foundation for positive change. When paired with strategic policies that increase housing supply, encourage responsible development, and support first-time buyers, rate cuts can play a significant role in making homeownership more accessible for Canadians.

Ensuring that rate cuts benefit those who need them most requires a balanced approach. Policymakers can further enhance affordability by implementing measures such as incentives for affordable housing development, streamlined zoning policies, and programs that encourage responsible homeownership. A lower interest rate environment makes it easier for both private and nonprofit developers to build, but sustained government support will be key to maximizing these benefits.

Looking ahead, the path to greater affordability will depend on continued collaboration between the public and private sectors. While unexpected challenges may arise, historical trends indicate that lower borrowing costs generally lead to increased development and better access to housing. By leveraging this opportunity wisely, Canada can take meaningful steps toward a more sustainable and inclusive housing market.